Promissory Note

A promissory note is a written and enforceable agreement in which a borrower promises to pay a lender a sum of money on demand, or within a specified period of time. The note records information about how much was lent (the principal amount), interest rates, when the payment is due (maturity date), when and where it was issued, and signatures.

A promissory note is also referred to as a:

- Debt Note

- Demand Note

- Commercial Paper

- Notes Payable

€120,00

When to Use a Promissory Note

If you’re borrowing or lending money, you should create a promissory note that addresses payment details, interest rates, collateral, and late fees. There are many types of promissory notes that can be used for several purposes, such as:

- Personal loans between family members, friends, and colleagues

- Student loans

- Real estate loans, property down payments, or mortgages

- Automobile, vehicle, or car loans

- Bank, commercial, business, or investment loans

In general, you should use a promissory note for more straightforward loans with basic repayment structures, and a loan agreement for more complex loans.

2. How to Write a Promissory Note

A legal promissory note should contain the following details and clauses:

1. Full names of parties (“borrower” and “lender”)

A standard promissory note should name who is receiving money or a line of credit (the “borrower”) and who will be repaid (the “lender”). Only the borrower must sign the promissory note, but it’s good practice to also include the lender’s signature.

- The lender may also be called a “payee”, “seller”, “issuer”, or “maker”.

- The borrower may also be called a “payer” or “buyer”.

2. Repayment amount (“principal” and “interest”)

All promissory notes, no matter how simple, should clearly state the amount of money being borrowed (the “principal” amount) that needs to be paid back. You also need to decide whether or not to charge interest, and how often it will be compounded (monthly or yearly).

If you’re unsure what interest rate to charge, visit the Wells Fargo Rate and Payment Calculator, Prosper Loans, or the Lending Club for a comparison of current interest rates for personal loans. You can use any of their promissory note amortization calculators to calculate the principal and interest payments on a monthly basis for the lifetime of the loan. Note: the majority of states have usury laws that restrict the interest rate you can charge.

For example, in California and Texas, a promissory note’s interest rate cannot exceed 10%. In comparison, Florida promissory notes can incur an interest rate of 18% (for amounts less than $500,000), or 45% (for loans greater than $500,000). Make sure you check the interest requirements in your state before drafting your loan notes.

Payments on the note are usually applied first toward the interest with the remainder applied toward the principal amount.

4. Payment plan

The promissory note should clearly spell out how the money will be paid back to the lender. For instance, depending on how the promissory note is structured, the borrower must pay back the lender by a certain date (known as a “maturity date”). If there is no date or if the date has already passed, it is “payable on demand” or “due on demand.” For all of the repayment options, refer to the table below.

Four Types of Repayment Options

5. Consequences of non-payment (“default” and “collection”)

If the borrower is unable to pay back the money on time and defaults on the note, the lender can enforce the promissory note and demand the full amount be paid, or collect on the collateral. If the borrower refuses to pay, the promissory note provides strong evidence if the lender wishes to initiate legal action. In the event that the borrower loses the lawsuit, they would also be responsible for paying any reasonable costs associated with the collection of debts, including attorney fees.

In the event that a borrower enlists a professional collection agency, they’ll be charged either a flat fee or a percentage of the outstanding debt. As a result, it’s sometimes in the lender’s interest to negotiate a debt settlement agreement with the borrower, and accept less than the original amount owed.

6. Notarization (if necessary)

Typically, a promissory note does not need to be notarized. However, always consult your local and state laws to verify signature and witness requirements.

7. Other common details

A promissory note may include these additional provisions:

- Acceleration: can the lender demand immediate payment from the borrower?

- Possible events of acceleration include:

- if the borrower becomes bankrupt

- if the borrower fails to make payments

- if the borrower passes away (i.e., death)

- if the borrower wants to pay off the note early

- if the borrower sells of a large or material portion of their assets

- Possible events of acceleration include:

- Amendment: any changes made to the note (must be done in writing)

- Collateral: if the borrower defaults, the lender can keep the designated collateral property

- Governing Law: which state’s laws apply

- Joint and Several Liability: all co-borrowers share responsibility

- Late Charges: a penalty is charged if the amount is paid back late

- Prepayment: the borrower can pay off the debt and interest early

- Right to Transfer: the lender can transfer the promissory letter to a different party

Once you’ve ironed out the details, give a copy of the signed promissory note to all involved parties, and then file the original in a secure location.

3. Free Promissory Note Template

Download a free promissory note template below. You can choose to make it either secured, or unsecured:

- Secured Promissory Note: Use this document if you want the borrower to agree to give up property (like jewelry, cars, businesses, or stocks) if they fail to pay back the loan.

- Unsecured Promissory Note: Use this document if you don’t want the borrower to agree to give up property if they fail to pay back the loan. Lenders will often demand higher interest rates in return.

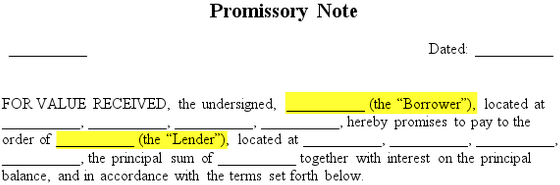

PROMISSORY NOTE

__________ Dated:_________

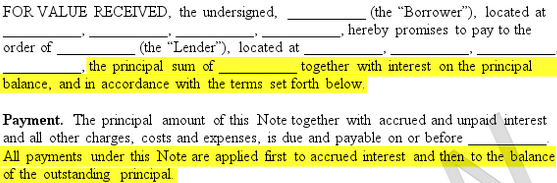

FOR VALUE RECEIVED, the undersigned, __________ (“Borrower”), hereby promises to pay to the order of __________ (“Lender”), the principal sum of __________ (the “Principal Amount”) in accordance with the terms set forth below.

- Payment. The Principal Amount together with all other charges, costs and expenses, is due and payable .

- Late Fee. If Borrower fails to make a payment due under this Note within __________ days after the due date, Borrower agrees to pay to Lender a late payment fee of __________.

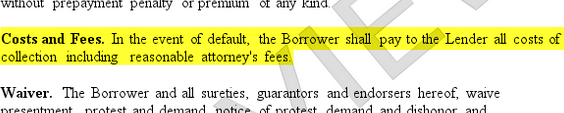

- Costs and Fees. Upon the occurrence of a default by Borrower, Borrower shall pay to Lender all costs of collection, including reasonable attorney’s fees.

- Waiver. Borrower and all sureties, guarantors and endorsers hereof, waive presentment, protest and demand, notice of protest, demand and dishonor and nonpayment of this Note.

- Assignment. Borrower may not assign its rights or delegate its duties under this Note without Lender’s prior written consent.

- Amendment. This Note may be amended or modified only by a written agreement signed by Borrower and Lender.

- Notifications. Any notice or communication under this Note must be in writing and either personally delivered, sent by overnight courier service, certified or registered mail, postage prepaid, return receipt requested or by facsimile or electronic email transmission.

- Governing Law. This Note shall be governed by and construed in accordance with the laws of the State of __________.

- Miscellaneous. This Note will inure to the benefit of and be binding on the respective successors and permitted assigns of Lender and Borrower. Lender shall not be deemed to have waived any provision of this Note or the exercise of any rights held under this Note unless such waiver is made expressly and in writing. Waiver by Lender of a breach or violation of any provision of this Note shall not constitute a waiver of any other subsequent breach or violation.In the event that any of the provisions of this Note are held to be invalid or unenforceable in whole or in part, the remaining provisions shall not be affected and shall continue to be valid and enforceable as though the invalid or unenforceable parts had not been included in this Note.

IN WITNESS WHEREOF, the undersigned has executed this Note as of the date first stated above.

SIGNATURES

___________________

Borrower Signature

___________________

Borrower Full Name

4. Promissory Note FAQs

The following are some frequently asked questions and answers about promissory notes.

What is the difference between an individual and an entity?

The borrower or lender can be either an individual (person) or an entity (company). Examples of an entity include a corporation, LLC, or partnership. In the case where either the borrower or lender is an entity, a representative must sign on the entity’s behalf.

What information should I include about the lender?

Include the lender’s full name and address as part of the contact information to be listed on the document. The lender is the person or company lending a sum of money to the borrower.

Can there be more than one lender?

Yes, if there is more than one lender, the additional lenders’ names should be listed on the promissory note.

Can I sell or transfer my promissory note?

A promissory note can serve as a substitute for money and can be transferred between lenders.

Another distinctive feature is that they can be transferred or treated as a “negotiable instrument.” If state requirements are properly satisfied, a note can be transferable or be exchanged between different parties, serving as a substitute for money.

Imagine Betty borrows $100,000 from Larry to start her very own 3D printing studio. The note requires Betty to pay Larry $1,500 every month ($500 goes towards an annual 6% interest rate and $1000 goes towards the principal) for 100 months until the balance is paid off. After 20 months of Betty diligently repaying, Larry actually would prefer to get his money back sooner so he can invest in an exciting dog walking business.

Instead of simply waiting for the maturity date of the note to arrive, Larry could sell his note for the remaining balance ($80,000 in principal plus $40,000 in interest payments yet to come) at a discount (maybe $90,000) to his friend Lisa who is happy to patiently accept Betty’s $1,500 monthly payments for the next 80 months (and make $30,000).

Each state regulates whether notes are transferable so be sure to consult your local laws and include the precise language needed (i.e. the note is made “payable to order” or “payable to the bearer”).

What are some of the tax benefits of a promissory note?

There may be situations where you want to clearly document whether the money being given should be treated as a gift or loan for accounting or tax purposes. For instance, the IRS allows you to give a gift of $14,000 to each of your very lucky family members for the year of 2015 without incurring gift tax consequences (i.e. annual gift tax exemption). Every year, for example, your grandparents could give a combined $28,000 to each of their grandchildren per year in an effort to reduce their estate taxes.

Similarly, spouses (including same-sex spouses!) may gift one another $14,000 per year and claim the gift tax marital deduction.

Transfers of money that fall under the annual gift tax exemption do not count towards your lifetime gift exemption of $5.45 million.

Additionally, educational tuition expenses or medical expenses paid directly on behalf of someone do not count towards the $14,000 per year gift limit. Because the IRS applies a hefty 40% gift and estate tax, refer to this Schwab article for a quick overview of estate planning tips and gift tax limits. Also, be sure to visit the IRS website for Frequently Asked Questions on Gift Taxes.

If you’ve already maxed out your giving (i.e. the annual gift tax exemption of $14,000 per person per year), you can help a family member in need by turning to the de facto “family bank” and using a promissory note. An intra-family personal loan, however, is subject to the minimum IRS Applicable Federal Rates (“AFR rates”), which are published monthly. Fortunately, the IRS required AFR interest rates are often below commercial mortgage rates, and all the interest and principal payments stay within the family. For comparison, consult this Small Business Lending Survey which is updated on a quarterly basis.

As an example, here are the annual AFR rates or minimum allowable interest rate required for a family loan using this document:

| SHORT-TERM LOAN < 3 YEARS |

MID-TERM LOAN 3-9 YEARS |

LONG-TERM LOAN > 9 YEARS |

|

|---|---|---|---|

| JUNE 2016 | 0.64% | 1.41% | 2.24% |

| MAY 2016 | 0.67% | 1.43% | 2.24% |

| APRIL 2016 | 0.70% | 1.45% | 2.25% |

As you can guess, the IRS is trying to distinguish between a genuine loan between family members and a gift from one family member to another disguised as a loan. In order to satisfy the stringent IRS guidelines, intra-family loans should be clearly documented with formalities like a note. This article by Investment News explains how this document can help families transfer wealth through more sophisticated intra-family loans.

What is the difference between an individual and an entity?

The borrower or lender can be either an individual (person) or an entity (company). Examples of an entity include a corporation, LLC, or partnership. In the case where either the borrower or lender is an entity, a representative must sign on the entity’s behalf.

What information should I include about the borrower?

Include the borrower’s full name and address as part of the contact information to be listed on the note. The borrower is the person or company borrowing a sum of money from the lender, to be repaid later.

Can there be more than one borrower?

Yes, if there is more than one borrower, the additional borrowers’ names will be listed on the note.

Do I need a cosigner or guarantor?

A cosigner or guarantor is optional and protects the lender in case the borrower defaults. The lender may require a cosigner if the borrower is in questionable financial standing. The cosigner is someone who jointly signs the agreement with the borrower.

In case the borrower defaults and cannot pay back the amount in full, the cosigner is responsible for paying back the lender for the amount due. The cosigner is usually someone in good financial standing or has excellent credit.

What payment information is needed for the terms of a promissory note?

The lender must indicate the amount of the note (called the principal), the interest rate, and the repayment method and schedule that the borrower will use to repay the loan amount. It is also best to include any additional stipulations, such as prepayment or default of the loan.

What are the options for paying back a loan?

The loan can be repaid in installments or at one time.

With an installment payment option (“Installment Payments”), the borrower repays the lender in a set number of installments over a set period of time as specified in the document. “Installment Payment with a Final Balloon Payment” is the same (repaying the loan in periodic installments), with the addition of one large “balloon” payment to be paid on the final due date.

If the loan will be repaid at one time, it can be repaid either on a specified due date or “on demand” by the lender. With a “Due on Demand” payment option, the borrower repays the lender upon the request and at the demand of the lender.

What is collateral and is it required?

The collateral is any asset that is worth the equivalent or more of the loan. It is optional to have the note require collateral from the borrower. Collateral acts as a type of protection for the lender in case the borrower defaults or fails to pay back the loan.

How much is the interest rate on a note?

Interest rate is governed by state law, so it is best to check your local or state law for the maximum allowable interest rate.

What is prepayment of the loan?

Prepayment is an option for the borrower to repay the loan, at any time earlier than the due date. The Borrower has the right to prepay all or any part of the loan at any time and without penalty. However, the Lender may require the Borrower to first provide written notice.

What happens if the Borrower misses a payment or pays late?

You can specify any or all of the communication methods listed (in person, e-mail, fax) or enter your own. If you want to limit the methods of communication, then choose only the ones that you would like to use.

What methods of communication can I specify?

You can specify any or all of the communication methods listed (in person, e-mail, fax) or enter your own. If you want to limit the methods of communication, then choose only the ones that you would like to use.

When should I include a signature for the lender?

By default, only the borrower’s signature is required. Including the lender’s signature is optional. If both parties wish to sign the document, then include the signature for the lender.

Specification: Promissory Note

|

User Reviews

Be the first to review “Promissory Note”

Vendor Information

- No ratings found yet!

There are no reviews yet.